The Game of Soybeans:

Emerging Supply from South America

By Dr. Scott B. MacDonald

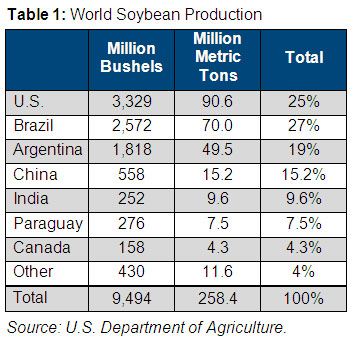

NEW YORK, NY (KWR) March 9, 2012 It has become a cliché to say that food is power. Yet, with seven billion people on the planet and more to come, even a cliché has meaning. One of the more widely consumed foods is the soybean. It is used to feed people directly, disguised into any number of other "foods," turned into edible oil, given to livestock that produce meat, and can be used as a source of energy. In 2010, soybeans represented 58% of world oilseed production and 35% of those soybeans were produced in the United States. According to Soy Stats, the United States exported 1.59 billion bushels (43.3 million metric tons of soybeans), which accounted for 44% of the world's soybean trade. While the U.S. is the leading producer of soybeans, it does not have the stage to itself. Argentina, Uruguay, Paraguay and Brazil increasingly carry weight. Indeed, part of the new geo-politics of food is being played out in South America.

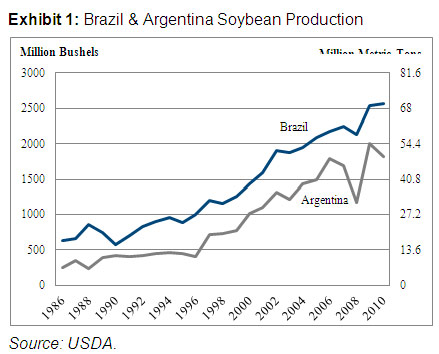

Argentina and Brazil have emerged as the powerhouses of soybean production outside of the United States. Expanded production since the mid-1980s has been considerable, as new lands have been opened up and transportation infrastructure upgraded to meet growing demand, especially from China. Indeed, it is China's voracious appetite that is changing the geo-political structure in South America.

The combination of Argentina, Brazil and Paraguay accounted for 50% of world soybean exports in 2010. Brazil alone accounted for 33%, making it the number two global player in soybean exports. This is a lucrative business. For the U.S., soybean and soy product exports were in excess of $23 billion in 2010, with China being the number one customer with $10.8 billion in ourchases. The same trends are evident in Argentina and Brazil, with China being the most significant buyer of soybeans and soy products.

Demand for soy and other food stock is not going away anytime soon, though prices are likely to see volatility. The key reasons for this are well-known:

Population growth is continuing. There are seven billion people now; the world's population is expanding by around 80 million people per annum. By the end of the 21st century, there is forecast to be more than nine billion people. They will need food;

Improving living standards through much of the developing world are causing greater demand for meat and dairy products as well as vegetable oils. The animals necessary for dairy products and meat have to be fed one outlet for soybeans, and in some cases, cooked, hence the need for vegetable oil;

The search for alternative sources of energy away from fossil fuels has turned to biofuels. Renewable energy is sexy and grains fit that category;

-

The financial element driven by the need for returns has pushed investors into commodity markets. These investments have grown substantially, with an estimated $412 billion (Q1 2011) being allocated in this area.

The boom in agriculture, particularly soybeans, is changing South America. Brazil, Argentina and Paraguay have already become more deeply linked to the global market. As production is expanding, Bolivia, Colombia and Uruguay are also being pulled into new arrangements. This means that the agricultural elites in these countries (i.e. the farmers) are gaining greater economic power and, with that, are articulating their own vision of national interests, which sometimes collide (as in Argentina) with the traditional, more urban political elite.

Looking ahead, there are three things investors should consider in looking at soybeans and the sustainability of South American production. First and foremost, South America has more room to grow more crops. As global population is set to expand, the world will have to produce more food. The World Bank (2010) released a "conservative estimate" that six million hectares of cropland would be added to the world's supply every year through 2010. In that calculation, Latin America accounted for one-third of that total. It should be noted that beyond the core South American producers of Argentina, Brazil and Paraguay, production is rising in places such as Peru, Colombia and Venezuela. Related to the land issue is that South America has the necessary water resources for the irrigation of soybean crops. As Mariano Turzi, a professor of international studies at Argentina's Torcuato Di Tella University and New York University Buenos Aires, noted: "The continent enjoys a freshwater resource ratio of more than 10,000 cubic meters per person annually, while Europe, China and India range from 1,700 to 3,900."

The second thing is Sino-American relations are likely to remain challenging in the decades ahead. While China is the major holder of U.S. government debt, the U.S. is one of the major sources of food for China. Neither country likes such vulnerabilities as they imply leverage. China was not pleased by the Obama administration's strategic reassessment to focus on the Asia-Pacific, which strongly implied China as the main rival to U.S. national interests. Chinese military doctrine is also clear as to the threat implied by the U.S. Consequently, China has been active in diversifying its food supplies, a strategy that has brought it to South America's soybean producers.

In an excellent article entitled "Grown in the Cone: South America's Soybean Boom," Current History (February 2012), Professor Turzi captures a major change in global geo-politics: "Will the rising powers of the twenty-first century China in particular view South American food production as among their core strategic interests? To what extent will China's relations with Latin American soy explorers resemble those between the U.S. and the Middle East's oil explorers?"

Considering how China is forced to deal with water issues, desertification in its north and a historical memory of great famines (the last occurring under Mao Zedong in the late 1950s-early 1960s), food security is an issue. Moreover, the present political system is based on a compact between the Chinese Communist Party and the population we will provide the citizen with a good standard of living, including food, and the citizen will support the ruling elite and generally stay out of politics. Failure to deliver could produce social instability, the critical lynchpin for change in dynastic China.

The third thing is the increasing push to secure prime agricultural-producing lands. This is not something being done solely by China. In his article, Turzi notes the following:

In December 2010, a lease agreement was signed between the Argentina province of Río Negro and the Chinese state-owned agricultural conglomerate Beidahuang Group. The deal includes an initial $20 million investment, with an estimated total of $1.45 billion over 20 years. Under the deal's provisions, a total of 320,000 hectares of farmland will be leased to produce soybeans, wheat and oilseed ripe to be shipped directly to China.

In April 2011, Chongqing Grain Group announced a $2.5 billion investment in an industrial soybean-processing complex in the Brazilian state of Bahia.

Indian companies are said to be looking at Argentinean land, while Brazilian companies have been reported to be looking at farmland in Angola to help meet growing demand. On the Indian side, Olam International acquired 17,000 hectares in Argentina to grow peanuts; the Solvent Extractors' Association of India (a consortium of 18 vegetable oil companies) has acquired land in Uruguay and Paraguay to grow soybeans and sunflowers; and Adani Group is planning to set up farms to cultivate edible oils in Argentina and Brazil (along with Africa).

The intensification of competition over soybeans and productive land is only going to escalate in the decades to come. It will pit governments and their agents against multinational companies like Archer Daniels Midland, Bunge and Cargill and will most likely create a new set of relationships between China and the Southern Cone, with implications for the rest of the world.

Changes such as these offer opportunities, both from a national view and from an investor standpoint. The countries in the soy-zone can leverage their international standing, while investors can look to purchases of agricultural land as a means of becoming more involved. The development of the soy-zone is going to be a long-term trend, something that will see more changes in geo-political arrangements. These can work for the better.

While the information and opinions contained within have been compiled from sources believed to be reliable, KWR does not represent that it is accurate or complete and it should be relied on as such. Accordingly, nothing in this article shall be construed as offering a guarantee of the accuracy or completeness of the information contained herein, or as an offer or solicitation with respect to the purchase or sale of any security. All opinions and estimates are subject to change without notice. KWR staff, consultants and contributors to the KWR International Advisor may at any time have a long or short position in any security or option mentioned.

KWR International Advisor

Editor: Dr. Scott B. MacDonald, Sr. Consultant

Deputy Editors: Dr. Jonathan Lemco, Director and Sr. Consultant and Robert Windorf, Senior Consultant

Publisher: Keith W. Rabin, President

To obtain your free subscription to the KWR International Advisor,

please click here to register for the KWR Advisor mailing list

For information concerning advertising, please contact:

Advertising@kwrintl.com

Please forward all feedback, comments and submission and reproduction requests to:

KWR.Advisor@kwrintl.com

Website content © KWR International